💸 HOW TO ROB SOMEONE IN BROAD DAYLIGHT

Why understanding the UK’s changing money rules matters more than ever

When a government needs more money, it really only has three choices:

1️⃣ Raise taxes

2️⃣ Borrow more

3️⃣ Cut spending

Borrowing isn’t easy because — just like people have credit scores — countries have credit ratings. If that rating drops, borrowing gets more expensive for everyone.

And cutting spending is never popular.

So most of the action ends up happening quietly through rule changes, not big, dramatic tax hikes.

This year’s Autumn Budget is a clear example of that.

Let’s break down the changes that will affect the most people, in plain English.

1. 🧊 THE INCOME TAX FREEZE: A QUIET, MASSIVE TAX RISE

The UK uses a progressive tax system (your income is taxed in slices).

In a fair system, these bands rise with inflation.

But we’ve seen:

Tax bands frozen since 2021

Meant to stay frozen until 2028

Now frozen until 2030/31

Meanwhile:

Prices up

Inflation up

Wages up just to survive

…but the tax bands stayed still.

Examples:

🧍 Someone earning £49,000

A normal 5% inflation pay rise increases their salary to £51,450.

That pushes them over the higher-rate threshold — into the 40% tax bracket for the first time.

Not because they’re better off.

Simply because the band didn’t move.

🧍♂️ Someone earning £52,000

A 5% rise takes them to £54,600.

Now an even bigger slice is taxed at 40%.

Again — costs are up too.

But their tax bill rises faster.

This slow creep is called fiscal drag,

and the government expects it to raise £8.3bn in 2029–30.

2. 🏦 SALARY SACRIFICE GETTING CAPPED (FROM APRIL 2029)

Salary sacrifice has long been a smart tax-saving method:

Pay directly into pension

Lower your taxable income

Save Income Tax and National Insurance

From April 2029:

Only the first £2,000 per year will keep the National Insurance saving.

Everything above that gets treated like normal pay for NI.

Still useful.

Just less powerful.

3. 📈 SAVINGS, DIVIDENDS & RENTAL INCOME — A LONG, QUIET SQUEEZE

This Budget didn’t introduce anything shocking in this area —

but it continued a pattern we’ve been seeing for years:

the government gradually tightening the rules around income that isn’t your salary.

Let’s break it down properly.

💰 Savings interest

The tax rate on savings interest hasn’t increased

But interest rates went up a lot in the last two years

Which means people are earning more on their savings

Meanwhile, the Personal Savings Allowance has stayed exactly the same:

£1,000 for basic-rate taxpayers

£500 for higher-rate

£0 for additional-rate

➡️ So more people are now paying tax on their savings simply because the allowance hasn’t changed while interest payments have increased.

The tax rate didn’t rise —

but the tax bill did.

📊 Dividend income

This one has seen clear policy tightening:

The dividend allowance used to be £5,000

Then it dropped to £2,000

Now it’s £500

And on top of smaller allowances, dividend tax rates for basic and higher-rate taxpayers have been increased in this Budget.

➡️ Even modest dividend income will now be taxed — and taxed more heavily than before.

🏠 Rental income

The squeeze on landlords has been happening for nearly a decade:

Mortgage interest relief removed

Wear-and-tear allowances removed

Higher borrowing costs

More compliance requirements

And now, an additional tax increase on rental profits

➡️ Rental income has progressively become less tax-efficient year after year.

⭐ The main point

None of this happened suddenly.

There wasn’t one big “tax hike”.

Instead, the government has been slowly reducing allowances and tightening rules,

so that income outside your salary — savings, dividends, rent — is taxed more often and more heavily.

4. 🏡 THE £2M PROPERTY SURCHARGE — CHEEKY, BUT IMPORTANT

This won’t affect most people (yet 😉) —

but the design of it is worth noting.

From April 2028, homes worth over £2m will be charged:

£2,500–£7,500 a year, rising with value

It appears on your council tax bill

But the money goes to central government — not your local council

So it:

Looks like council tax

Is paid like council tax

But is actually a central-government tax in disguise

🔥 That’s the cheeky part.

And remember:

You can be asset rich and cash poor.

You might inherit a property or live somewhere that shot up in value.

And yes — future me, who enjoys looking at nice houses for inspiration — already feels attacked. 😅

5. ⚖️ THE BIGGER ISSUE: INCENTIVES ARE STARTING TO FEEL WEAK

Across all these changes, one theme appears:

You earn more → you lose more

You save more → more gets taxed

You invest → more gets taxed

You rent out property → more gets taxed

You use smart strategies → the rules tighten

It’s not just about the money.

It’s about the signal.

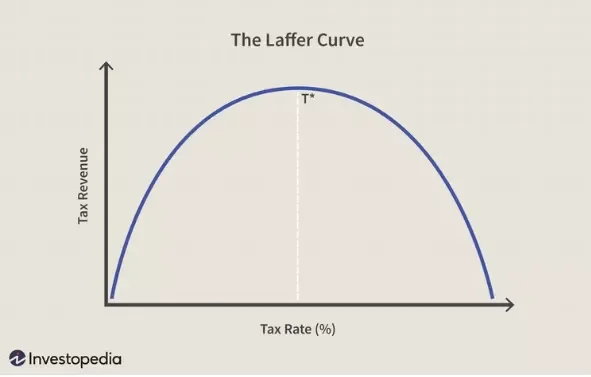

And this is where the Laffer Curve comes in.

The Laffer Curve is an economic principle that basically says there comes a point where, if taxes feel too high or too heavy, people work less, invest less and take fewer risks — and the government ends up collecting less, not more.

A country that needs energy, ambition and innovation can’t afford dull incentives.

6. 📘 MONEY MADE CLEAR LAUNCHING….

Policies will always change.

But the principles of wealth building don’t.

That’s why I’m launching:

💡 MONEY MADE CLEAR — a 6-week game-changing programme designed to elevate your financial habits, sharpen your wealth strategy, and set you up for long-term success.

We’ll break down:

How to build an emergency fund

How to manage cashflow and budgeting

How investing actually works

Insurance, protection & wills

Long-term planning

The principles of wealth creation that work anywhere

And so much more…

📩 There’s a big early-bird discount for those who join this year.

If you want to step into 2026 feeling more prepared, more confident and more in control of your money, send me a message and I’ll send you the early details.

The rules will keep changing —

but once you understand the fundamentals, you will stay ahead.